|

A collective but contrasting dive into the phase of world geopolitical dislocation.

by GEAB (GlobalEurope Anticipation Bulletin) October 16, 2010

In this issue, our team introduces the annual "country risk" update in the light of the crisis. Based on an analysis incorporating eleven criteria this year, this decision-making tool has already demonstrated its relevance in faithfully anticipating developments over these past twelve months.

The identification, at the beginning of 2009, of a new phase of the crisis (the phase of global geopolitical dislocation) forced us to take new parameters into account (nine indicators were selected in 2009) to effectively incorporate trends that are reshaping the global system (1). As 2010 draws to a close, LEAP/E2020 now estimates that the world’s various countries are heading for a collective dive at the core of this phase of socio-economic and strategic geopolitical dislocation (2). Thus our studies enabled us to continue presenting the LEAP/E2020 anticipation of "country risk" for the 2010-2014 period (3), by adapting the categories to the crisis’ development, via four groups of countries (4) characterized by the contrasting impacts of this dive in the geopolitical dislocation phase of the global systemic crisis (5).

On the other hand, in this GEAB issue, we give our anticipations for the progress of Euro-Russian relations between now and 2014. In our recommendations, we pay particular attention to helping our readers deal with a currency market in global conflict, a fallout anticipated over 18 months ago by our team, as a result of geopolitical dislocation. Moreover, on the occasion of the publication of his book "The Global Crisis: The Path to the World After - France, Europe and the World in the 2010-2020 decade ", Franck Biancheri, Director of LEAP/E2020, and Anticipolis editions, have given us permission to publish his analysis of the process of the ongoing global geopolitical dislocation.

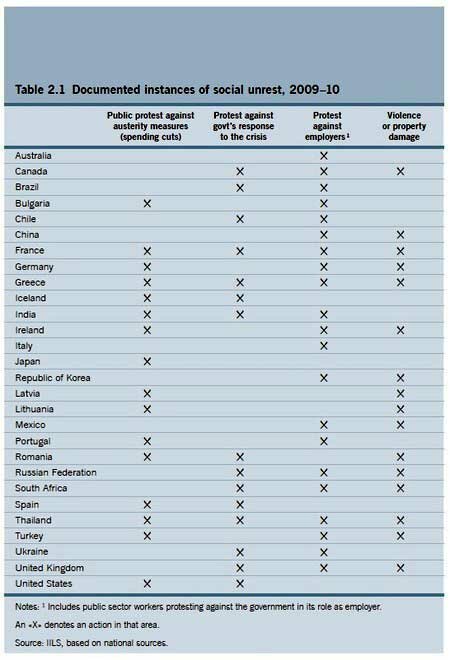

Documented instances of social unrest 2009-2010 - Source: IILS, 09/2010

The G20’s (or IMF’s) now patent failure to secure effective international cooperation to try and remedy the structural weaknesses of the current international monetary system perfectly illustrates LEAP/E2020’s anticipation which in March 2009, before the London G20 meeting, explained that the summit was the only window of opportunity to fundamentally rethink the global monetary system at the heart of the current crisis. In failing to seize this opportunity, we reported that the world would begin to enter the global geopolitical dislocation phase from late 2009. At that time, by way of an introduction to this new phase of the crisis, the world has seen the mid-flight explosion, during the Copenhagen summit, of the whole international process on global warming. Since then, every month brings a stream of public finance crises in one state or another, drastic austerity measures causing increase in social unrest (6), international meetings leading to reports of disagreement, the proliferation of threats between States over trade imbalances, etc., all against a background of a downward spiral into hell of the global system’s central power, namely the United States (7).

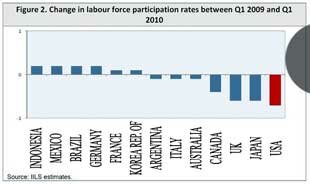

Change in labour force participation between the first quarters of 2009 and 2010 (Indonesia, Mexico, Brazil, Germany, France, South Korea, Argentina, Italy, Canada, United Kingdom, Japan and the United States) - Source: IILS, 09/2010

For several months now we have been witnessing the onset of a massive currency world war just like LEAP/E2020 anticipated nearly two years ago and reiterated in its time-frame of the crisis (8). Several weeks hence, the inevitable failure (9) of the FMI/G20 duo to resolve these currency-trade (10) tensions will provide both new evidence while marking a new tipping point of global geopolitical dislocation: every man for himself becoming the rule (11).

Two weeks from now, with the announcement of the actual details of a comprehensive plan to reduce spending, the United Kingdom will eventually have to face an unprecedented (12) socio-economic crisis that it has desperately tried to hide for months (13), and it will have to do it alone (since the United States are unable to help it, and it has put itself outside the European financial rescue system).

And in three weeks, the United States will concurrently expose an unprecedented political paralysis following the mid-term election (14), whilst the US Federal Reserve will launch a new attempt to rescue the US economy by monetizing a stimulus plan that the federal government is no longer able to launch (15). This attempt - whose size will be less than financial markets expect (because the Fed is now forced, in this case by the holders of US Dollar denominated assets: China, Japan, Europe, oil-producing countries (16)...) but more than enough to lead to a further fall in the dollar and plunge the world monetary system into an even worse conflict - will fail anyway because US society has, de facto, entered a phase of austerity that US leaders, in 2011, will have to recognize must also constrain the country’s fiscal and monetary policy (17).

From the world leaders’ side (18), the next four years’ global sequence can be summarized quite simply: last US attempts to "return to the world before the crisis" (stimulating consumption, maintaining deficits, debt monetization) that will all fail (19), last Western attempts to deal with the crisis using "Washington consensus" methods (limiting deficits by reducing social spending, no tax increases on high incomes, privatization of public services, ...) which will generate growing socio-political chaos, acceleration of the BRIC countries’ exit from the majority of Western financial and monetary markets (especially the two financial pillars of Wall Street and London) which will increase monetary instability, rising intensity of trade wars (coextensive with currency wars (20)), the coming to power from 2012 of groups of leaders who have decided to try new solutions (21) to exit the social, economic and political consequences of the crisis, taking note of the fact that the “Washington consensus” is dead ... because there is no consensus anymore and because Washington is a moribund world power.

As for the rest, the keeping the US debt’s Triple-A rating belongs to the same virtual world as the recent declaration by US economic authorities (22) of the end of recession: the growing disconnect between the words of a collapsing system’s key players and the reality perceived by the majority of citizens and socio-economic players is an infallible indication of systemic decline (23). But the financial markets are not mistaken because with the soaring cost of insuring US debt hot on the heels of Ireland and Portugal with a 28% third quarter increase in cost, the United States has become the third country for which the debt markets fear some very unpleasant surprises (24).

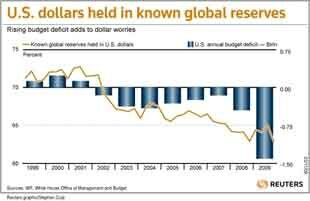

Comparative progression of the United States’ deficit (in trillions USD) and the amount of known global reserves held in U.S. Dollars (1999-2009) - Sources: Reuters/IMF/White House OMB, 10/2010

---------

Notes:

(1) From the beginning of 2006, in the GEAB No. 5, LEAP/E2020 indicated that the global systemic crisis would evolve in 4 major phases. "A global systemic crisis develops in a complex process that can be cut into four phases which may overlap:

. a first "trigger" phase that suddenly sees a whole series of factors, hitherto disconnected, start to converge and interact, and which mainly remain noticeable to alert watchers and the main players

. a second phase called "acceleration" which is characterized by the sudden realization by the vast majority of players and observers that the crisis is here because it starts affecting a rapidly growing number of the system’s elements

. a third "impact" phase which is formed by the radical transformation of the system itself (implosion and/or explosion) under the effect of accumulated factors and which simultaneously affects the entire system

. and finally, a fourth phase called "decanting" that sees the release of the new system’s characteristics resulting from the crisis. Source GEAB No. 5, 15/05/2006

. early 2009, in the GEAB No. 32, LEAP/E2020 identified a fifth phase of the crisis, called global geopolitical dislocation, which begins at the end of 2009, following the G20 failure to launch a credible process of establishing a new international system, particularly in the monetary field. This new phase has been, of course, integrated into the time-frame presented last year in GEAB No. 38.

(2) The ability of states to cope with social unrest that will multiply in the coming quarters and years is closely linked to their ability to contain the most traumatic social effects of the crisis; therefore, our team has introduced a tenth indicator correlated to the tax burden of the past twenty years, whilst an eleventh indicator has been added to assess the resilience to a global monetary war.

(3) Our team has analyzed indicators for 39 countries in addition to Euroland.

(4) These country- risk analyses may be particularly useful for those planning an investment in a given country, intending to settle there or wishing to make an investment in assets linked to that country.

(5) We chose to keep 2014 as an overview because we believe that the changes in political leadership occurring in many important countries (China, USA, Russia, France, ...) in 2012, and which are the principal potential positive factor looking at the next four years, will have no appreciable impact on these country-risks before 2014, the time that new policies are starting to yield results.

(6) France gives a striking example with the growing unpopularity of an executive which fails to prevent social unrest against its reforms and which risks turning into a general strike (France 24, 14/10/2010). Meanwhile, throughout Europe, there is a marked increase of extremist political forces. Source: Le Point, 20/09/2010

(7) All the lights are turning red. The road transport volume has started to decline again (Los Angeles Times, 13/10/2010). Foreclosures continued to grow last month, whilst the whole legal system on which they rest has now broken down (for the legal reasons mentioned in the GEAB a year ago) upsetting a real estate market on Fed and Federal Government life support even more (CNBC, 14/10/2010; USAToday, 14/10/2010; USAToday, 11/10/2010). Cities are sinking into vey deep deficits (such as their employee retirement funds estimated at over 500 billion USD, CNBC/FT, 12/10/2010) and are obliged to turn to the states to try and extricate themselves (CNBC/NYT, 05/10/2010), while the latter can no longer balance their budgets and are obliged to pay interest rates higher than developing countries (thus, Illinois must now pay more than Mexico to borrow, Bloomberg, 05/10/2010).

(8) See the GEAB N°43 particularly.

(9) History doesn’t repeat itself. If we pushed so hard (including at the cost of a full page advertisement in the global edition of the Financial Times) for world leaders to seize the opportunity at the G20 in Spring 2009, it was because we were aware that such a set-up would not happen again. Now the US is too weak to continue to steer the global game, no other player is able to take affairs in hand ... and therefore, the global financial system looks more and more like the "drunken boat; in Rimbaud's poem describing the drift towards unexplored beaches, a perfect description of the world’s course today.

(10) As for the negotiations on climate change, a "West" already clearly divided (here between the Dollar, Pound, Yen and Euro), tries to make the emerging countries (the Yuan in particular) pay the cost of adapting a system they invented and which no longer works. And it's not by ending the game as shown by US efforts to prevent any new Chinese rating agency from operating in the United States that will dissipate this feeling in the BRIC countries. One remembers the performance in Copenhagen. It will pale in comparison to what awaits us at the G20 meeting in Seoul. Besides, the soaring gold price is a very reliable indicator: even the European central banks have stopped their sales. Sources: New York Times, 21/09/2010; Vigile, 29/09/2010; PrisonPlanet/FT, 27/09/2010, Bloomberg, 10/10/2010; ChinaDaily, 27/09/2010

(11) The Telegraph summarized it admirably on 11/10/2010 in "Jobless America threatens to sweep us all away." Sign of the times, Bloomberg on 08/09/2010 announces the opening of a Ruble-Yuan currency exchange in Shanghai to finance Sino-Russian trade.

(12) There is a growing fear in the United Kingdom over the country’s social and political situation in the context of "super-austerity" planned by the government due to financial and budget crisis: the loss of nearly a million jobs, social crisis, unrest.... Sources: Independent, 02/10/2010; Telegraph, 13/10/2010; Guardian, 11/09/2010; MarketWatch, 21/09/2010.

(13) This was, moreover, the main reason for the “Greek crisis becoming the Euro crisis” in Spring 2010, in particular fed daily by articles in the Financial Times to divert attention from London and the Pound Sterling. See GEAB in the first half of 2010.

(14) Recent statements by Steve Schwarzman, head of the financial giant Blackstone, comparing Barack Obama's willingness to tax financial companies more heavily to Hitler’s invasion of Poland, illustrates the explosive atmosphere that rules at the core of the US elite. Source: NewYorkPost, 14/10/2010

(15) Because of the magnitude of existing deficits and political deadlock in Washington.

(16) In this regard, our team gives a timely reminder that there is no mystery about the simultaneous rise of different asset classes, like stocks or gold for example: operators are leaving the stock exchanges (as we showed in the last GEAB issue) and selling their financial and monetary assets for gold (or other less dangerous assets) and the Fed (and its partners) are injecting liquidity into the financial markets to prevent a widespread collapse. The only problem, when the music stops: it will be a tragedy for the stock exchanges. Source: CNBC, 08/10/2010

(17) The situation is so bad that a reading of the New York Times of 13/10/2010 started to look like a cut and paste of the GEAB a year or two ago ... that’s saying something! The article by Michael Powell and Motoko Rich, which describes the "recovery" as merely a continuation of this recession shows the plight of the middle classes across the country in a harsh light, while the very same day Paul Reyes unveils a remarkable collection of photographs showing the ravages of the "Very Great US Depression" as LEAP/E2020 has called it since late 2006.

(18) Franck Biancheri offers a detailed presentation, with the two likely main scenarios for 2010-2020, in his book "The Global Crisis: The Path to the World after;

(19) Source: SeekingAlpha, 24/09/2010

(20) Singapore’s recent announcement that from now on its currency’s trading band against the U.S. dollar will be wider, is the latest example (each day brings a new one) of increasingly defensive positions taken by individual states. Each one tries to increase its room for maneuver to cope with the unexpected. Incidentally, it is interesting to note that Singapore suffered a 19% third quarter fall in GDP, evidence that the mood in Asia is becoming gloomy. Source: , 14/10/2010; MarketWatch, 13/10/2010

(21) For China, one solution will most probably be to inject the country's huge US Dollar reserves into the economy as already suggested by the new generation of Chinese bankers. This will not help the US Dollar. Source: Dallasnews, 19/09/2010

(22) The National Bureau of Economic Research (NBER is in charge of "holding a Mass" on this subject.

(23) As MSNBC aptly described on 06/10/2010, it’s once a month at midnight that America’s great depression is revealed in the supermarkets, when tens of millions of food voucher recipients go and do their shopping. According to the study by the Center for Economic and Policy Research published on 16/09/2010, in effect now one in three Americans can no longer make ends meet (one hundred million people ).

(24) Source: CNNMoney, 12/10/2010

|

|

|